I’m sure you have heard quite a bit about credit. Good credit, bad credit. But what exactly is credit?

Quick answer: “Credit” generally refers to your credit score, which is a number that grades you on how risky it may be to give you a loan.

Having good credit means that you are expected to be a responsible money borrower- you will probably pay your loans back in full and on time. Good credit is often rewarded with the ability to borrow more money and lower interest rates on loans (you REALLY want this, because of compound interest!)

Bad credit means you are considered a higher risk loan customer. It might be harder for you to get a loan, and your interest rates will probably be higher than someone with good credit.

So what is a credit score? A credit score is a number between 300 and 850. Seems crappy that all of your brains and beauty and talent should be simplified into one measly number, but that’s how life works sometimes. Try to get the best number you can!

- Below 600 is generally considered not so hot. You might have trouble getting a loan and your interest rates will not be great.

- 600-674 is below average.

- 675-710 is good.

- 710 and above is excellent. You should have no trouble getting a loan and you should be able to get highly competitive interest rates.

How do you find your credit report?

Under law, you can get a free summary of your credit report once a year. There is only one website that is authorized to give you the official credit report that you are legally entitled to. This is https://www.annualcreditreport.com/. They get their data from one of three sources and you can pick one to give you your free report: Equifax, Experian or TransUnion. Any other website has not been Federally approved and are considered scam websites (and you are putting your social security number in there, so be careful!).

Equifax, Experian and Transunion get their data from different sources, so theoretically your credit reports could be different from each company. You can only order from one of these companies each year for free, but you can always pay for reports from the other two companies.

It’s important to get your credit report periodically because it helps you make sure the information is accurate. It also protects you against identity theft.

What is in a credit report?

Information such as: your address, social security number, date of birth (to make sure it is you!).

How much credit you have access to (loans, credit cards, mortgages etc.) and the dates of opening these accounts.

How many loans you have requested (signing up for lots of credit cards can impact you negatively!)

Any outstanding debt or collections you have against you.

If information is not correct on the report, you can follow these instructions for getting it fixed. If this happens to you, I am sorry about the additional paperwork.

Is my credit score on the report?

Drat! No! You usually have to pay more (between $10 and $15) to get your credit score. If you are thinking about taking out a big loan in the future, it is probably worth your money to pay for the credit score so you can factor interest rates into your budget. I get mine every few years just to check in, because there are ways you can improve your credit score if you need to.

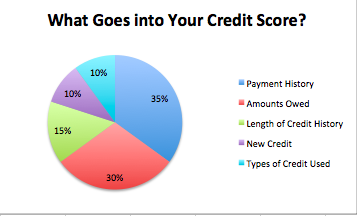

What impacts your credit?

Payment History

I hope by now you have already automated your bill payments so you know that 35% of your credit score is PERFECT!

If you had some errors in the past, those problems may stay on your report for up to 7 years. Sorry. If you are currently in a dispute over a bill or if you just missed one payment, make sure you call to ask that the late payment isn’t reported. Usually there is a grace period and you won’t get reported if it has only happened once, so don’t freak out. Also sometimes (for whatever reason this happens with medical bills frequently) the first time I get the bill in the mail it is already overdue. Just pay it as soon as you get it and save the envelope with the postage date stamp- they will send you second and third notices before they actually report you for nonpayment.

A benefit to being young: if you make a lot of credit errors when you are 21 (we all made a lot of mistakes when we were 21, don’t worry. Tequila was high on my list…), by the time you are ready to buy a house, you will probably have moved past the seven year mark and your errors will be off of your credit report. It is not as easy for a 35 year old to recover from credit mistakes because a 35 year old generally needs access to more credit than someone in their early 20s.

Amount Owed

The amount owed does not necessarily mean that if you are in debt, you have bad credit. It really refers to a how much you owe compared with how much people would loan you. If you have a credit card with a $15,000 limit and you owe $2,000, you still have $13,000 of credit available. That is good. If you have a credit card with a limit of $5,000 and you owe $2,000, you only have $3,000 left of credit. That isn’t so great.

One way to improve your credit score (immediately! One phone call!) is to ask for a credit increase. This is only appropriate for you to do if you don’t have a ton of credit cards and/or loans out, because asking for too much new credit at once can harm your credit report. (GAH! Can we never win!?!) But occasionally- maybe once a year, or if you get a raise- call up your credit card and ask for a credit increase.

Length of Credit History

This one is pretty obvious- the longer you have been using credit and paying bills on time, the safer a candidate you are. If you are a freshly minted adult, now is a good time to slowly start using credit to build up a good credit history. Additionally, if you have a credit card that you never use but you have had for a long time- don’t close that account. Keep it open (maybe put your Netflix subscription on there and automatically pay it off each month, so you don’t have to think about it).

Also- closing an account does not delete it from your credit history. Sorry, kids.

New Credit

If you have suddenly signed up for four credit cards all in the same day (did you get suckered into those 20% off offers at the mall?!?!! NOOOOOOOOOOO!!!!!) then your credit score will suffer (especially if you don’t have a long credit history). Any sudden request for multiple forms of credit may drop your score.

This is why I NEVER recommend that people sign up for those store credit cards at the mall. Saving 20% on a pair of sweet shoes may save you $20 today, but a lower credit score can impact your mortgage rates when you buy a house, which will cost you THOUSANDS OF DOLLARS. You should have two or three credit cards, but you should not have a different credit card for every store you have ever shopped in. It is better to have a few credit cards with high credit limits and rewards you like.

Types of Credit

Your score also considers the different types of credit you have. Credit cards, installment loans, retail accounts, mortgages, car loans are all different types of loans. It’s normal for young people to only have a credit card and not a mortgage, so don’t go buying a car to try to diversify your loan types. It is more important that you are responsible for the types of credit that you do have, so that when you get older and buy a house you will already have a solid credit score to negotiate with.

There you go: credit demystified. Not as scary as it seems, huh?

Reblogged this on twentiesinyourpocket and commented:

I’ve started volunteering as a personal finance educator, and a lot of the questions I get are about credit- here is some information for y’all!

LikeLike